Table of Contents

2026 Calgary Housing Market Forecast: Trends & Predictions

As the Calgary housing market continues to evolve, understanding its complexities is crucial. This guide offers insights into the trends and expectations shaping the future of Calgary’s real estate market.

The Calgary real estate market in 2026 is characterized by a weaker economic backdrop most notably weak population growth and raising unemployment. Rising inventories a stubbornly high days on market will remain seasonally elevated for the duration of the 2026. Calgary’s housing market will be unusually divided between single-detached and multi-family homes, with the latter at high risk of more severe price declines

Delve deeper into what 2026 may hold for Calgary’s housing market. Covering economic influences, property trends, and predictions, this guide provides comprehensive insights for homeowners, investors, and industry professionals.

Benchmark Price

—

Benchmark price: $—

- YoY —

- MoM —

Absorption Rate

—

Absorption Rate: —

- MoM —

- —

Quick Overview

2026 Calgary Housing Market Forecast: Calgary is likely to move through a more balanced, slower-growth market in 2026, with more buyer leverage than the past couple of years. Our equal-weight Alberta economic index has cooled from recent highs and the 9-month RSI (measure of trend strength) is entering the lower band, which historically aligns with slowing demand, higher inventory, and longer days on market rather than rapid price acceleration.

Base case (most likely): flat to low single-digit change in home prices, with conditions favoring well-priced listings and stronger negotiation room on overstretched sellers. Late 2026 could mark the bottom for prices with early 2027 beginning the recovery.

Best case (still realistic): low single-digit price growth if borrowing costs ease gradually, sales activity firms up, and population inflows remain steady—tightening inventory in the most in-demand segments (detached and well-located family homes) while condos/townhomes stay closer to balanced. Winter of 2026 could mark the bottom for the Calgary real estate market and spring 2026 could offer low price appreciation lead by detached homes.

Worst case (still realistic): mid to low single digit decline if rates stay higher for longer, job growth softens, and inventory builds faster than seasonal demand. In this scenario, the market becomes very price‑sensitive, days on market remain above 40, and sellers in oversupplied segments face the most pressure to reduce. Weakness would likely extend well into 2027.

What could change the outlook of the Calgary real estate market: Cooling inflation leading to faster‑than‑expected rate cuts, a renewed migration surge, or a major energy/commodity upside shock could tighten inventory again and push pricing back into stronger growth.

Key Drivers of Calgary’s Housing Market

How Alberta’s Economy Shapes Calgary Real Estate

Alberta’s economy shows weakness with low consumer spending and business activity, but showed some signs of strength in the latest manufacturing data. The Calgary housing market is heavily tied to several key provincial economic indicators each with a 80% or higher correlation to Calgary sold prices. These indicators give us the best crystal ball to predict future pricing.

Our model integrates seven key provincial economic indicators, most closely linked to Calgary’s real estate market, to form an equally weighted index. This indicator correctly tracked the 2024 housing peak, and subsequent 2025 pricing slump. The indicator has broken below 2022 levels and predicts further weakness for at least the next 6-12 months. Below is a snapshot of our Alberta Economic Index.

Alberta’s Labour Market and Wage Trends

Alberta’s labour market has remained relatively resilient, but it can still send mixed signals month to month as higher borrowing costs and input costs work through the economy. Wage growth supports household incomes, yet it can also increase pressure on business margins—sometimes leading employers to trim non‑essential roles while keeping core staff. This is especially evident in very high unemployment amongst youth. This trend will likely be made worse as businesses begin rapid adoption of Ai.

This presents an interesting market setup that could see Calgary real estate communities with a higher percentage of renters or lower-income support staff being more heavily impacted by Ai—particularly in condo and multi-family properties.

Population Trends and Demand for Calgary Housing

Alberta’s population growth is still a major demand driver for Calgary housing, but heading into 2026 the trend is much weaker than the surge of the past couple of years. Federal immigration planning has shifted toward lower permanent-resident targets versus prior “record-high” plans, and policy is increasingly aimed at restoring balance in overall newcomer volumes.

That doesn’t mean demand disappears—Calgary can still attract newcomers because it remains relatively affordable compared with other major cities—but the market will be less defined by extreme inventory-crunch conditions for some time.

Net Migration (10-Year)

Net migration is the number of people moving in minus moving out. Higher readings typically support housing demand; falling readings can signal cooling demand.

| Period | Net migration |

|---|

Global & National Forces Impacting Calgary’s Market

Global and national headlines matter for Calgary—but the transmission into Alberta usually runs through migration, energy prices, the Canadian dollar, and business confidence.

1) Trade war and tariffs: If global trade friction escalates (especially U.S. policy shifts), Alberta is most affected when it changes the outlook for North American growth and energy demand. Tariffs can also raise costs for construction materials and equipment, which tends to keep replacement costs elevated—even in a softer resale market. The bigger risk is uncertainty: businesses pause hiring and investment when the rules keep changing.

2) Canadian dollar (CAD): A weaker CAD is a two-sided story for Alberta. It can support commodity-linked revenues (since oil is priced in U.S. dollars) and it can make Canada feel “cheaper” for newcomers with USD savings. But it can also push up the cost of imported goods and building inputs. For housing, the net effect often shows up as a mix of supportive income backdrop with stubborn build costs—not necessarily instant price spikes.

3) Oil prices: Oil remains Alberta’s high-impact lever. When oil prices (and expectations) rise, Alberta typically sees stronger corporate cash flow, hiring plans, and in-migration—supporting housing demand in Calgary. When oil weakens, the housing market can cool through slower job momentum and softer confidence. The key nuance: Calgary doesn’t need “booming oil” to stay stable—it just tends to accelerate when energy is a tailwind.

Practical takeaway for 2026: with the economic index cooling, Calgary’s base case stays more balanced—but a meaningful upside or downside swing in oil and trade policy can still change sentiment and demand faster than most local indicators.

Seasonal Trends in Calgary Real Estate Market

Ten years of historical patterns show Calgary’s housing demand is highly seasonal—your 10‑year composite demand index is strongest in late winter / spring, then fades into year‑end.

Monthly Demand Trends

Strongest months:March–June (peak typically March, remaining elevated through June)

Still positive:February, July–October (cooler but generally supportive)

Weakest months:January, November–December (December is typically the softest)

How to use this for 2026

If the broader economic backdrop stays balanced (as our index suggests), seasonality can matter even more:

Sellers: the best odds of multiple‑offer energy are usually Feb–Jun (with March often the hottest). If you’re selling in Q4, plan for sharper pricing and stronger prep/marketing.

Buyers: the best negotiation windows tend to be late fall and winter (Nov–Jan) when demand is weakest and listing competition thins.

Practical strategy: if you’re buying in spring, tighten your criteria early and get fully prepared; if you’re buying in Q4/Q1, focus on disciplined offers and longer negotiations.

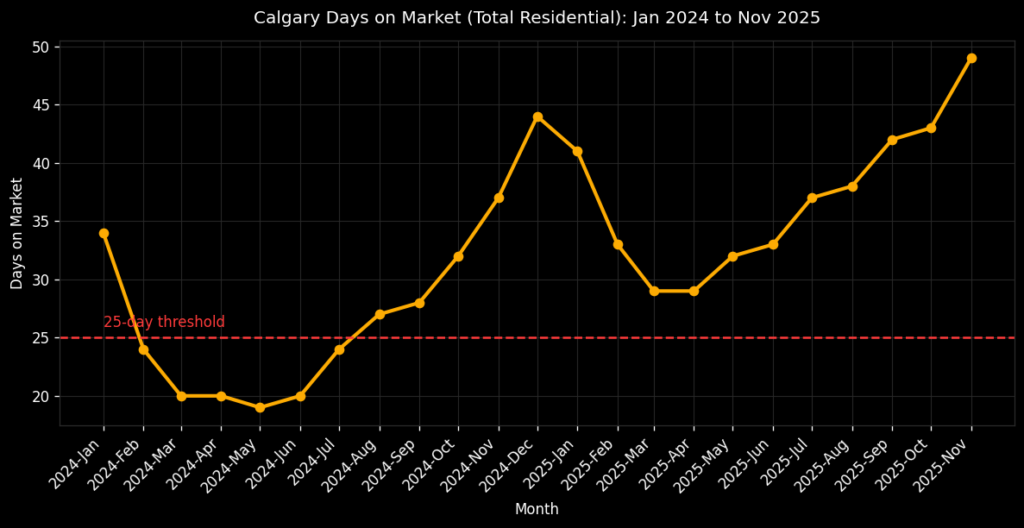

Days on Market: A Key Indicator for 2026

Our analysis identifies days on market as one of the most predictive local indicators for the direction of Calgary’s real estate market. Based on our projected trend, days on market for detached homes was expected to peak in January 2026 and then ease, falling below 40 days by March 2026—offering some relief for sellers who had experienced sustained month-over-month price declines.

However, our model also anticipates a sharp reversal beginning in mid 2026, with days on market resuming an upward trend. How high this indicator rises by Dec 2026 will be key to determining whether 2026 marks a bottom—or whether market weakness extends into 2027.

In our framework, meaningful price appreciation typically requires days on market to remain below 25 days for at least two consecutive months. Currently, Calgary’s days on market is approaching 50, which supports a more cautious pricing outlook in the near term.

Inventory and Supply Trends in Calgary

Economic data shows that inventory is still 28% higher than last year, and supply gains are mostly in row and apartment units. Overall net migration is substantially lower than it was during 2024.

When months of supply is closer to 2, sellers have more negotiating power. As it pushes toward 3–5 (and beyond), buyers gain leverage—especially in the segments with the most supply (new communities apartments, and row housing). Housing price appreciation highly correlated to provincial migration trends.

New listings: 2,251 (-3.3% YoY)

Inventory: 5,581 (+28.2% YoY)

Months of supply: 3.59 (up from 2.43)

Housing Affordability in Calgary

Calgary’s 2026 housing market is shaped by shifting affordability and a changing balance of power between buyers and sellers. While Calgary remains more affordable than many other major Canadian cities, buyers are facing new challenges as household incomes, mortgage rates, and property prices adjust to economic headwinds.

Canadian Housing Snapshot (Major Cities)

Avg. sold prices • Latest available: Nov 2025

| City | Market Trend | Avg. Home Price | Detached | Attached | Apartment |

|---|---|---|---|---|---|

| Calgary | Balanced | $615,986 | $755,596 | $446,304 | $359,761 |

| Vancouver (Metro) | Decreasing | $1,235,575 | $2,025,115 | $1,224,509 | $791,229 |

| Winnipeg | Decreasing | $373,642 | $420,121 | $356,847 | $272,718 |

| Ottawa | Increasing | $683,783 | $834,489 | $543,777 | $452,668 |

| Toronto (GTA) | Decreasing | $1,039,458 | $1,346,017 | $913,078 | $663,290 |

| Hamilton | Decreasing | $746,377 | $818,353 | $632,903 | $387,113 |

Buyer and Seller Dynamics in 2026

Inventory levels have climbed sharply, with supply up 28% year-over-year and most of the gains concentrated in row and apartment units. This increase in available homes—combined with softer net migration and cautious buyer demand—has tipped many market segments toward more balanced or even buyer-leaning conditions. For sellers, this means pricing competitively and being prepared for longer days on market, especially in higher-density property types.

The months of supply now sits at 3.59, up from 2.43 a year ago. Historically, when months of supply rises above 3, buyers gain more leverage in negotiations, particularly for condos and townhouses where inventory is highest. Detached homes and well-located family properties remain relatively resilient, but even here, buyers are finding more options and improved bargaining power compared to the ultra-competitive conditions of recent years.

For first-time buyers, these dynamics offer both opportunities and obstacles. While entry-level condos remain within reach for households earning around the median Calgary income, affordability for single-family homes has become more challenging. Buyers should be prepared to act strategically—taking advantage of increased selection and negotiating room, but also mindful of potential competition in the most desirable segments.

Overall, 2026 is expected to be a year where affordability and market balance are in flux, requiring both buyers and sellers to adapt their expectations and strategies to Calgary’s evolving real estate landscape.

2026 Outlook by Property Type: Detached, Condo, Townhouse, and New Builds

Detached Benchmark Price

—

Detached Benchmark Price: $—

- YoY —

- MoM —

Semi-Det. Benchmark Price

—

Semi-Detached Benchmark Price: $—

- YoY —

- MoM —

Apartment Benchmark Price

—

Apartment Benchmark Price: $—

- YoY —

- MoM —

Understanding the nuances of Calgary’s housing market requires a close look at how each property segment—detached homes, condos, townhouses, and new construction—is performing and what the outlook holds for 2026.

Detached Homes: Resilience Amid Shifting Conditions

Detached homes remain the most resilient segment in Calgary’s market. Despite broader economic headwinds and a cooling Alberta index, demand for well-located, family-oriented properties continues to outpace supply. Inventory for detached homes has risen, but not as sharply as in higher-density segments, keeping months of supply closer to balanced levels. While price growth has moderated, detached homes are expected to see flat prices in 2026, especially if borrowing costs ease or population inflows stabilize. Sellers in this segment still have some negotiating power, but buyers now benefit from more choice and less urgency than in previous years.

Condos and Townhouses: Increased Supply and Buyer Leverage

Condos and townhouses are experiencing the sharpest inventory gains, with supply up significantly year-over-year. This influx, combined with softer net migration, has shifted these segments firmly into buyer-friendly territory. Days on market are longer, and sellers face heightened competition—especially in newer developments and less central locations. Prices for condos and townhomes are under pressure, with a low single-digit decline or flat performance most likely in 2026. For buyers, this environment offers greater selection and negotiating room, but also requires discernment as some buildings may see further price softness.

New Construction: High Activity, Heightened Competition

New construction in Calgary is at record levels, particularly in higher-density formats such as apartments and row housing. Developers have responded to demand by bringing significant new supply to market, but sales activity has not kept pace. As a result, new builds—especially condos and townhomes—are seeing increased incentives and price adjustments to attract buyers. Detached new builds, while still in demand, face less pricing pressure but are not immune to broader market trends.

Segment Divergence and Strategic Opportunities

The divergence between detached and higher-density segments is likely to persist through 2026. Detached homes and well-located family properties are expected to lead any eventual recovery, while condos and townhouses may continue to face headwinds. Buyers and investors should pay close attention to inventory trends and days on market within each segment, as these are the clearest signals for future price movement and negotiation leverage.

In summary, Calgary’s housing market in 2026 will be defined by segment-specific dynamics: resilience and stability in detached homes, ongoing adjustment and opportunity in condos/townhomes, and a competitive environment in new construction. Understanding these nuances puts both buyers and sellers in a stronger position to navigate the year ahead.

More Articles

Content Sourcing

Written by licensed Calgary real estate professionals. Contact Us to learn more about our editorial standards. Information is based on publicly available data, local MLS® statistics, and professional experience in the Calgary real estate market.

About Us

- The 2% Realty Story

- How 2% Realty Works

- Our Google Reviews

- Fee Calculator

Calgary Real Estate

- Map of Calgary

- Monthly Market Update

Site Map & Terms